Public Exchange Subsidies – A Snapshot with Distant Clouds

By Clive Riddle, September 11, 2015

Two item of note occurred this week with respect to public exchange subsidies and enrollment: CMS released their June 30, 2015 Effectuated Enrollment Snapshot, and federal judge Rosemary Collyer in an unprecendented ruling that congress has standing for litigation, has allowed United States House of Representatives v. Burwell et al, U.S. District Court for the District of Columbia, No 14-1967 to move forward.

So the attempts to chip away at health insurance marketplace subsidies did not die with the Supreme Court ruling on King v. Burwell, and another cloud, albeit distant for now – as it will undoubtedly wind through an appeals process assuming it succeeds at Collyer’s level – hangs over the head of public exchange subsidies.

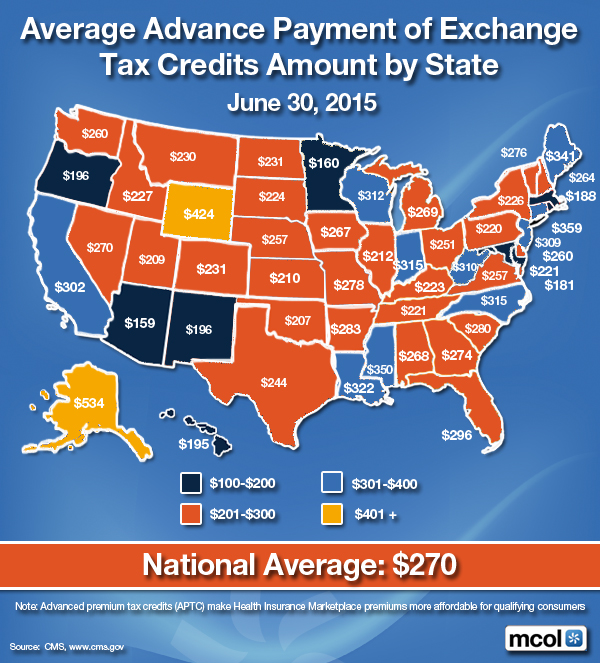

But in the meantime, CMS has provided a current picture of what these subsidies entail. CMS announced that “Of the approximately 9.9 million consumers nationwide with effectuated Marketplace enrollments at the end of June 2015, about 84 percent, or more than 8.3 million consumers, were receiving an advanced premium tax credit (APTC) to make their premiums more affordable throughout the year. The average APTC for those enrollees who qualified for the financial assistance was $270 per month. There were 7.2 million consumers with effectuated enrollments at the end of June 2015 through the 37 Federally-Facilitated Marketplaces (including State Partnership Marketplaces) and supported State-based Marketplaces (collectively known as HealthCare.gov states) and 2.7 million through the remaining State-based Marketplaces.”

Here is an infographoid MCOL will release next week, mapping the average subsidies by state:

CMS notes that “the ten states with the highest rate of consumers who received financial assistance through APTC were: Mississippi (95.4%), Wyoming (92.2%), North Carolina (91.6%), Florida (91.3%), Alabama (90.9%), Louisiana (90.7%), Georgia (90.0%), Arkansas (90.0%), Wisconsin (89.6%), and Alaska (88.8%). The states with the lowest rate of consumers who received APTC are: District of Columbia (10.2%), Minnesota (54.8%), Colorado (55.3%), Hawaii (61.4%), New Hampshire (62.8%), Vermont (64.2%), Utah (65.6%), Kentucky (69.8%), Maryland (70.7%), and New York (71.4%).”

With respect to enrollment by metal plan, CMS shared that 1% were enrolled in Catastrophic plans (63,174); 21% in Bronze plans (2,096,542), 68% in Silver plans (6,761,363); 7% in Gold plans (695,377); and 3% (332,624) in Platinum plans.

The issue of inappropriate marketplace enrollment has been increasingly raised by various parties. CMS released data regarding enrollment data matching initiatives, noting “During the time period from April 1, 2015 to June 30, 2015, enrollment in coverage through the Federally-facilitated Marketplaces was terminated for about 306,000 consumers with citizenship or immigration status data matching issues who failed to produce sufficient documentation of their citizenship or immigration status. In addition, during the same time period, about 734,000 households with annual household income inconsistencies had their APTC and/or CSRs for 2015 coverage adjusted. Overall, as of June 30, 2015 the Marketplace has ended 2015 coverage for approximately 423,000 consumers with 2015 coverage who failed to produce sufficient documentation on their citizenship or immigration status and has adjusted APTC and/or CSRs for about 967,000 households.”

Post a Comment By Riddle, Clive |

Post a Comment By Riddle, Clive |

Reader Comments